March 2026 Update – Middle East Conflict and Market Risk

Global geopolitical and economic uncertainty has unfortunately become a defining characteristic of the 2020s, the recent increase in military activity and geopolitical tensions in the Middle East being yet another example. The beginning of U.S. and Israeli military operations against Iran prompted swift retaliatory action, which included an attempted drone strike on Qatar’s energy infrastructure. While no damage was recorded, a major liquefied natural gas terminal was closed, signaling the potential for broader fallout than resulted from the June 2025 Israel -Iran conflict.

While North American equities have so far been relatively unaffected, there have been pronounced and intuitive reactions in other segments of the market. Oil and natural gas prices have jumped, while traditional safe-haven assets have also for the most part been acting rationally, with gold, silver, and the U.S. dollar all up. Global bond yields are one exception, having risen as of this writing. This dynamic potentially reflects heightened concerns about renewed inflation and the indirect impact it could have on future central bank decisions.

While there are clearly a lot of unknowns, we are currently focusing on three major variables in our effort to assess the potential market and economic implications of the conflict:

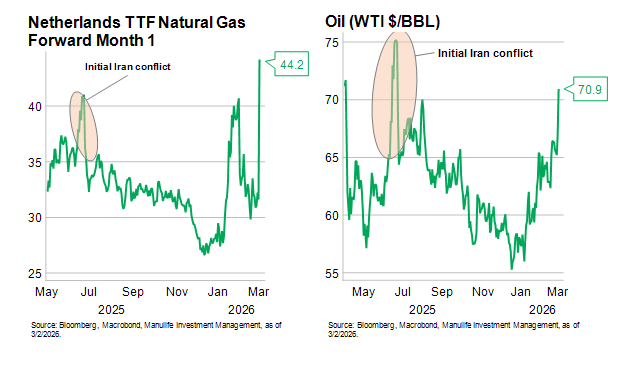

- Time. For now, our base case is that this latest episode will be relatively short-lived. Our rationale is simple: The Trump administration has developed a track record of fairly brief, focused military operations (e.g., Iran in June 2025 and Venezuela in January 2026). If that is indeed the case again this time, the direct economic impact would likely skew more toward temporary distortions than major inflection points, with markets quickly reverting to pre-war narratives. The most obvious historical comparison would be the price action for oil and natural gas during and after the U.S. and Israeli strikes on Iran in June 2025.

If the current conflict were to extend much longer than a few weeks, market and economic impacts could become more significant, with the relatively ‘benign’ outcome implyingsustained but somewhat moderate energy price increases. In that case, if only Iranianenergy production were disrupted, current excess global supply could somewhat mitigatethe disruption. However, other regions would probably be more vulnerable, includingcountries that rely directly on Iranian oil (e.g., China, India, and Asia more broadly). A larger concern would be the risk of wider global disruptions, at least partly due to some closure of the Strait of Hormuz, perhaps leading to a more pronounced move higher in energy prices. However, as long as military action stayed confined to military targets and didn’t affect energy infrastructure, a relatively prompt reversal could be plausible.

If the current conflict were to extend much longer than a few weeks, market and economic impacts could become more significant, with the relatively ‘benign’ outcome implyingsustained but somewhat moderate energy price increases. In that case, if only Iranianenergy production were disrupted, current excess global supply could somewhat mitigatethe disruption. However, other regions would probably be more vulnerable, includingcountries that rely directly on Iranian oil (e.g., China, India, and Asia more broadly). A larger concern would be the risk of wider global disruptions, at least partly due to some closure of the Strait of Hormuz, perhaps leading to a more pronounced move higher in energy prices. However, as long as military action stayed confined to military targets and didn’t affect energy infrastructure, a relatively prompt reversal could be plausible.

- Infrastructure. Energy prices would likely increase dramatically if commercial infrastructure (namely the energy production complex) were to be targeted and damaged/destroyed anywhere in the region. In this scenario, energy prices could surge and begin to weigh more heavily on economic growth, potentially contributing to a stagflationary environment. However, we place a somewhat lower probability on that outcome because any meaningful impairment would also affect Iran. (However, the likelihood could increase in line with any sense of Iran being ‘cornered.’)

- Escalation. The scope of the conflict has so far remained relatively contained and could remain so. If, however, Iran’s retaliation were to include the aforementioned energy complex, the use of proxies to expand the geographic scope of the conflict and/or hamper traffic through the Suez Canal, a broader and potentially more destructive regional spillover could occur, affecting not only energy prices but also global supply chains.

Alex Grassino, Global Chief Economist

Manulife Investment Management

Important disclosure:

Investing involves risks, including the potential loss of principal. Financial markets are volatile and can fluctuate significantly in response to company, industry, political, regulatory, market, or economicdevelopments. The information provided does not take into account the suitability, investment objectives, financial situation, or particular needs of any specific person. All overviews and commentary are intended to be general in nature and for current interest. While helpful, these overviews are no substitute for professional tax, investment or legal advice. Clients and prospects should seek professional advice for their particular situation. Neither Manulife Wealth and Asset Management, nor any of its affiliates or representatives (collectively “Manulife WAM”) is providing tax, investment or legal advice. This material is intended for the exclusive use of recipients in jurisdictions who are allowed to receive the material under their applicable law. The opinions expressed are those of the author(s) and are subject to change without notice. Our investment teams may hold different views and make different investment decisions. These opinions may not necessarily reflect the views of Manulife WAM. The information and/or analysis contained in this material has been compiled or arrived at from sources believed to be reliable, but Manulife WAM does not make any representation as to their accuracy, correctness, usefulness, or completeness and does not accept liability for any loss arising from the use of the information and/or analysis contained. The information in this material may contain projections or other forward-looking statements regarding future events, targets, management discipline, or other expectations, and is only current as of the date indicated. The information in this document, including statements concerning financial market trends, are based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. Manulife WAM disclaims any responsibility to update such information. Manulife WAM shall not assume any liability or responsibility for any direct or indirect loss or damage or any other consequence of any person acting or not acting in reliance on the information contained here. This material was prepared solely for informational purposes, does not constitute a recommendation, professional advice, an offer or an invitation by or on behalf of Manulife WAM to any person to buy or sell any security or adopt any investment approach, and is no indication of trading intent in any fund or account managed by Manulife WAM. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. Diversification or asset allocation doesn’t guarantee a profit or protect against the risk of loss in any market. Unless otherwise specified, all data is sourced from Manulife WAM. Past performance does not guarantee future results. This material has not been reviewed by, and is not registered with, any securities or other regulatory authority, and may, where appropriate, be distributed by Manulife WAM and its subsidiaries and affiliates. Manulife WAM is the global investment, financial advice, and retirement plan services segment of Manulife Financial Corporation.

© 2026 by Manulife Wealth and Asset Management. All rights reserved. The statements and opinions expressed in this article are those of the author. Manulife WAM cannot guarantee the accuracy or completeness of any statements or data.

5266935 3/26